How AI Tools Build Customized Financial Plans

Having a written financial plan has long been linked with greater confidence. Yet only 36% of Americans report having one, according to surveys, while 96% of those who do say it gives them reassurance about achieving long-term goals. Historically, creating such plans often meant long spreadsheets, manual projections, and repeated advisor meetings.

Now, AI-driven platforms like PortfolioPilot.com make it possible to assemble and adjust retirement strategies much more efficiently. These tools don’t just deliver a one-time plan—they allow people to test different scenarios and adapt to changing markets or personal circumstances.

Key Takeaways

- AI platforms integrate account data, goals, and economic inputs to design personalized retirement roadmaps.

- Scenario modeling helps explore different retirement ages, spending levels, withdrawal strategies, and tax decisions.

- Tools can incorporate assumptions about inflation, expected returns, and evolving risk tolerance.

- Some plans update dynamically, staying aligned as circumstances and markets shift.

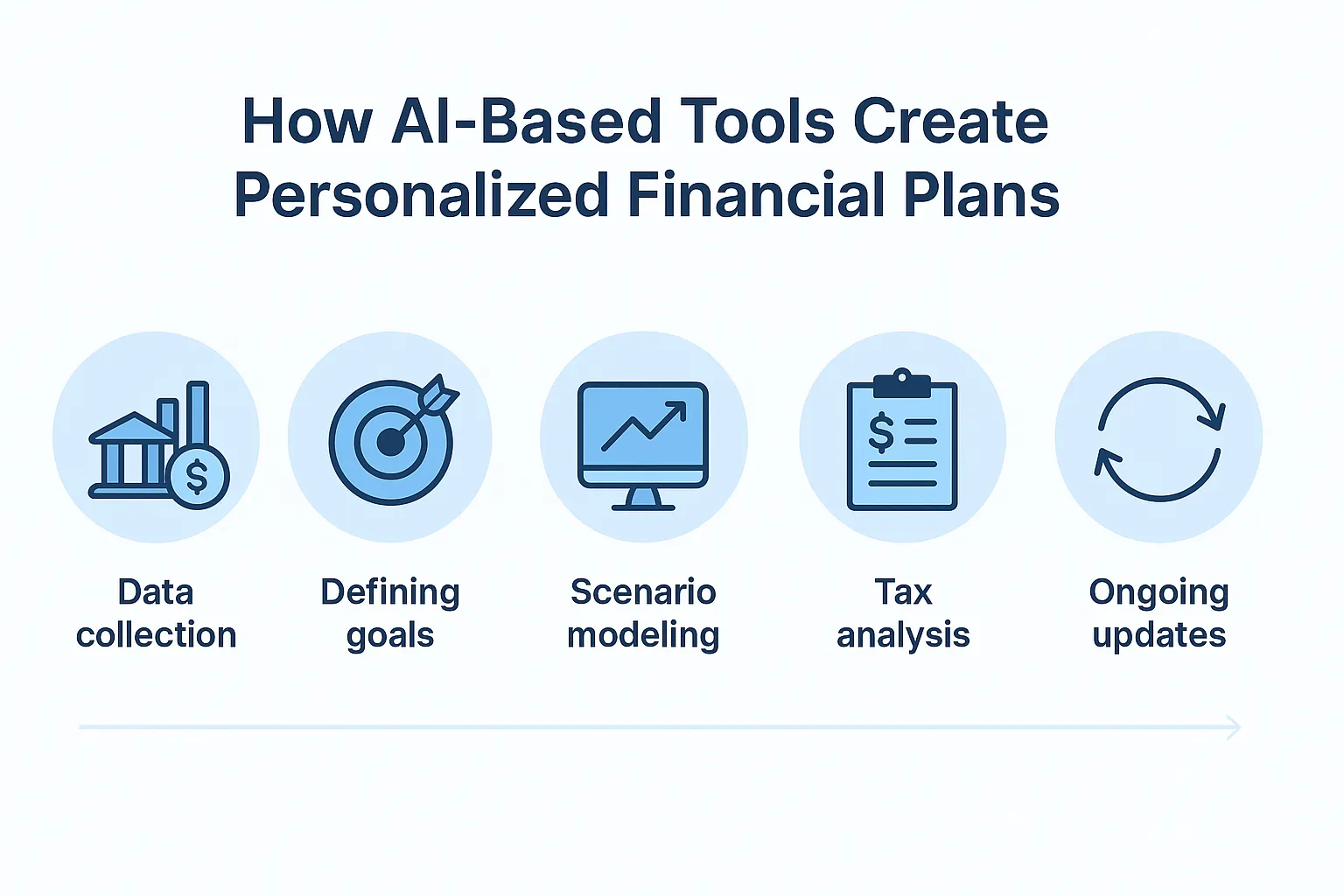

Step 1: Gathering Data and Linking Accounts

The first step is pulling together all financial information. AI planning platforms connect account balances, investment holdings, contribution rates, and debt obligations—across brokerage accounts, retirement plans, savings, and even real estate.

With this complete view, the tool can highlight:

- Heavy concentration in one asset class

- Unused tax-advantaged accounts

- Gaps relative

- to stated retirement goals

Why it matters: Plans built on partial data can miss important risks or opportunities. Full integration is the baseline for meaningful modeling.

Step 2: Setting Goals and Boundaries

Once the financial picture is clear, users define their personal objectives—such as target retirement age, desired annual income, or major future expenses like tuition or a new home. They also add limits like risk comfort, liquidity needs, or legacy intentions.

Hypothetical Example:

- Retire at age 62

- Annual income target: $90,000 in today’s dollars

- Leave $250,000 to heirs

This step ensures that projections reflect lifestyle priorities rather than broad averages.

Step 3: Scenario Testing and Simulations

One of the biggest strengths of AI platforms is running “what-if” models. Tools like PortfolioPilot test plans under a range of conditions: interest rate changes, inflation shocks, or market volatility.

Users can adjust:

- Retirement age

- Annual spending assumptions

- Contribution amounts

- Withdrawal methods

- Tax rules or expected asset growth

Hypothetical: A 45-year-old with $600,000 in savings might compare two scenarios—retiring at 65 with moderate expenses, or at 60 with higher travel costs. The AI can show success probabilities, how quickly assets may draw down, and potential tax impacts.

By comparing side by side, users see the trade-offs between retiring sooner and preserving long-term financial security.

Step 4: Evaluating Tax Effects

Taxes often represent one of the biggest costs in retirement. AI tools can model how different withdrawal orders—from taxable, tax-deferred, or Roth accounts—affect after-tax income.

They may also project the effect of Required Minimum Distributions (RMDs) and highlight years where Roth conversions could reduce future tax pressure.

- Why it matters: Understanding lifetime tax costs under different strategies can change how income is drawn over time.

Step 5: Keeping Plans Flexible

Life and markets rarely follow a straight line. The strongest AI planning tools allow users to revisit key assumptions—retirement age, spending levels, contributions, tax settings, and growth expectations—whenever needed.

This prevents the “set it and forget it” issue. A plan that looked sustainable in 2020, for example, might have needed updating after a sharp interest rate rise or an unexpected life event.

AI-based financial planning platforms are not about replacing long-term discipline with quick answers. They’re about keeping a plan current, helping people adjust when things change, and making the path to retirement easier to track.

The best results come when the strategy reflects both financial realities and personal goals. AI simply provides the framework for testing options, measuring trade-offs, and staying prepared for whatever comes next.