The Diversification Myth: When It Hurts More Than Helps

We’ve all heard it: “Don’t put all your eggs in one basket.” Diversification is the golden rule of investing, right? But what if we told you that too much diversification could actually be hurting your portfolio more than helping it?

Many investors are taught that diversification lowers risk—and that’s true, up to a point. But beyond a certain threshold, adding more assets can dilute your returns, increase complexity, and even introduce risks you didn’t intend to take.

In this article, we’re going to break down the diversification myth: why it exists, where it goes wrong, and how professionals often actually strike the right balance.

Key Takeaways

- Diversification can help reduce unsystematic (company-specific) risk, but can be overdone.

- Over-diversification can lead to index-like returns without the benefit of real control.

- Too many assets = complexity, overlap, and hidden correlation.

- Pros often focus on efficient diversification—not more, but smarter.

The Good Side of Diversification (At First)

Diversification typically works because it spreads your risk. Instead of betting on one company or one sector, you hold a mix of assets so that if one crashes, others might hold up—or even rise.

Hypothetical Example:

Let’s say you own only one stock—Tech Company. If Tech Company tanks, your entire portfolio suffers.

Now let’s say you own:

- 25% Tech Company

- 25% Bank Company

- 25% Utility Company

- 25% Health Company

Now you’ve diversified across sectors. A bad quarter in tech may be offset by gains in healthcare or utilities.

This is called reducing idiosyncratic risk—the risk tied to a specific company or industry. It’s a core principle of Modern Portfolio Theory (MPT), and it works.

But here’s where it goes wrong...

When Diversification Starts to Hurt

1. Diminishing Returns of Diversification

Once you own around 15 to 30 well-chosen stocks, you’ve already reduced many of the unsystematic risks in your portfolio. Adding more beyond this point offers diminishing marginal benefits. According to research from the CFA Institute, the incremental reduction in risk becomes negligible after this range—yet many investors still hold 100+ securities and overlapping funds, often duplicating exposure without improving diversification.

2. Dilution of High-Conviction Ideas

Diversification can make you feel safer, but too much of it can water down your best ideas.

Imagine you’ve identified five investments with strong return potential. But because you want to "stay diversified," you only give each 5% of your portfolio. That means even if one of them doubles, your portfolio barely moves.

Professionals often avoid this by concentrating capital where their conviction is strongest, while still managing risk.

3. Hidden Correlations

Just because two assets look different doesn’t mean they act differently under stress.

During crises—like 2008 or 2020—assets that were previously uncorrelated (like stocks and real estate) can suddenly move together. This phenomenon is known as correlation convergence.

So having dozens of different positions might not help if they all fall at the same time.

4. Complexity and Cost

More assets can mean:

- More trading and rebalancing

- More taxes

- More fees (especially in mutual funds or ETFs)

- More tracking headache

Simplicity can be a strength. Don’t confuse activity with effectiveness.

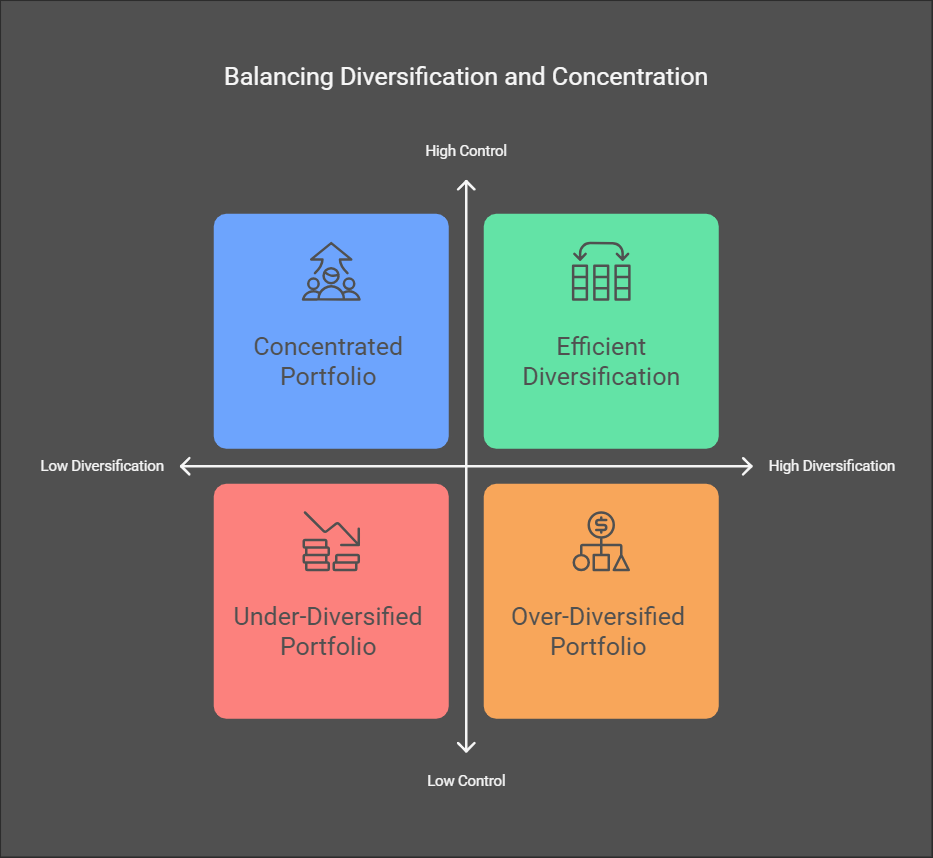

The chart below illustrates four common portfolio types based on diversification and control. It shows how investors often fall into the trap of over-diversifying or under-diversifying—and highlights why professionals commonly aim for the top right quadrant: efficient diversification.

Efficient portfolios strike a smart balance—broad enough to manage risk, but focused enough to deliver results.

The Professional Approach: Efficient Diversification

In our opinion, both individuals and portfolio managers should aim for efficient diversification—enough variety to reduce risk, but concentrated enough to generate meaningful returns.

Here’s what that looks like:

- Low Correlation, Not Just More Names

- Focus on adding assets that behave differently in various economic environments.

- Position Sizing with Purpose

- Don’t spread capital equally just for the sake of it. Size positions based on conviction, risk, and role in the portfolio.

- Use Asset Classes Strategically

- You can mix equities, bonds, commodities, real estate, and even cash to buffer against different risks.

- Stress Test Your Portfolio

- Use scenarios (e.g., interest rate spikes, recessions) to test whether your portfolio holds up when correlations rise.

How optimized is your portfolio?

PortfolioPilot is used by over 30,000 individuals in the US & Canada to analyze their portfolios of over $30 billion1. Discover your portfolio score now:

Analyze your entire net worth

360° portfolio analysis, AI Assistant, and personalized recommendations guided by our Economic Insights Engine.