How Much Does Tax Policy Drive Wealth Gaps?

According to Federal Reserve data, the share of aggregate US wealth held by the top 1% rose from about 28.1% in Q1 2009 to 30.4% in Q1 2019, while the bottom 50% held roughly 0.5% in Q1 2010 and only 1.6% in Q1 2019. Many assume tax policy is to blame. But the reality is more complex. This article examines whether tax rules, market dynamics, or structural ownership patterns play the bigger role in widening wealth gaps.

Key Takeaways

- Tax codes often favor capital over labor - through lower rates on capital gains and carried interest.

- Wealth inequality is also driven by who owns appreciating assets - not just tax treatment.

- Structural forces like stock buybacks, monetary policy, and financial literacy gaps shape outcomes.

- Some investors may benefit from understanding how these forces influence portfolio strategy and tax exposure.

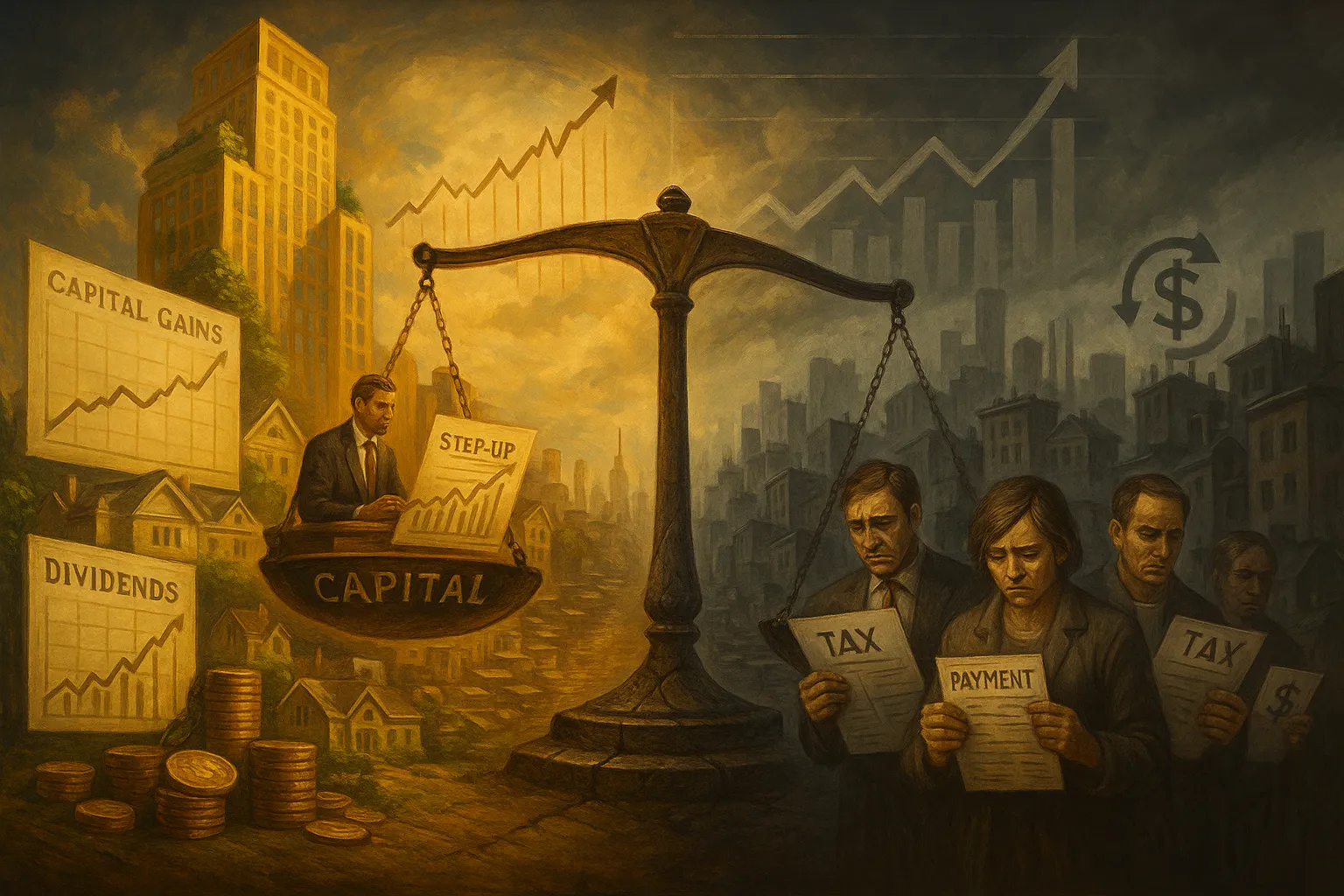

Why the Tax Debate Misses the Bigger Picture

Many people believe the rich don’t pay their fair share. While tax avoidance and loopholes do exist, they’re only part of the story. US tax policy includes lower rates on long-term capital gains, step-up in basis at death, and limited estate tax exposure. But these design choices affect people differently based on how they earn and hold wealth.

For example, someone who makes $500,000 in wages pays a higher effective tax rate than someone who sells $500,000 in appreciated stock held over a year. But only a small segment of the population holds significant appreciating assets.

According to the Federal Reserve, the top 10% of households hold over 88% of all US equity assets. That means even neutral tax rules often have unequal results.

- Hypothetical: Consider two families earning the same income. One rents and relies on wages; the other owns stocks and receives most income via dividends. Over 10 years, the second family not only builds equity, but pays a lower tax rate. Policy didn’t create the gap - but it reinforced it.

How Asset Ownership Shapes Outcomes

Ownership, not income, increasingly defines financial outcomes. Capital markets have been strong in recent decades, and those with access - via retirement accounts, brokerage holdings, or private equity - have disproportionately benefited.

For example:

- Homeowners build equity tax-free up to certain limits.

- Investors defer capital gains taxes until realization (or avoid them via basis step-ups).

- Pass-through businesses benefit from qualified business income (QBI) deductions.

These are legal and widely available, but they assume you have wealth to begin with. That’s where inequality compounds: people who own productive assets tend to stay ahead.

Monetary Policy and Market Mechanics

Tax policy doesn’t operate in a vacuum. Central bank actions also affect inequality.

During the 2020–2021 monetary easing cycle, the S&P 500 Information Technology sector delivered a 44% total return in 2020, while the S&P US REIT Net Total Return index posted a ~41.8% gain in 2021 - both performances underpinned by ultra-low interest rates and large-scale Fed asset purchases. Those already invested saw their portfolios surge, while others struggled with rising costs of living.

Similarly, corporate stock buybacks concentrate gains among shareholders. Since executives often hold equity, this can further increase top-tier wealth.

Between 2007 and 2016, S&P 500 companies distributed 96% of their net income through share buybacks and dividends.

So what? Understanding these forces helps investors assess where they fall on the spectrum—and what levers may exist within their own financial planning. Tax-smart portfolio construction, diversified ownership, and long-term strategies can mitigate some disparities.

Behavioral Blind Spots

Many people underestimate the compounding effect of small policy differences. For instance:

- Not maxing out a tax-deferred account can mean hundreds of thousands lost over time.

- Holding assets in taxable accounts without considering wash-sale rules or capital gains brackets may erode returns.

At the same time, it’s easy to overestimate what policy alone can change. Even progressive reforms may not close gaps if ownership remains uneven.

A small shift in asset mix or tax location - made consistently over years - often has more impact than waiting for legislation to catch up.

How optimized is your portfolio?

PortfolioPilot is used by over 40,000 individuals in the US & Canada to analyze their portfolios of over $30 billion1. Discover your portfolio score now:

PortfolioPilot users saved $11M+ on taxes in 2024

It’s simpler than you think. In just 5 minutes, you can find out if there are any tax-loss harvesting opportunities available.11