Common Mistake #22: Keeping an Emergency Fund in a Regular Checking Account

Emergency funds exist to absorb shocks. They provide liquidity when income is disrupted, expenses spike unexpectedly, or timing matters more than return. Because of that role, many investors default to keeping emergency reserves in regular checking accounts, assuming that maximum accessibility requires accepting zero return.

In practice, this choice often goes unexamined. Yet in periods when short-term interest rates are elevated, the gap between what emergency cash earns in a checking account and what it could earn in low-risk cash vehicles becomes meaningful. This article explains why keeping an emergency fund in a regular checking account is a common but inefficient habit, how it quietly reduces financial resilience, and how liquidity and interest are not mutually exclusive.

Key Takeaways

- Emergency funds prioritize liquidity, not inactivity.

- Keeping reserves in non-interest-bearing accounts creates avoidable drag.

- The difference between checking yields and cash yields compounds over time.

- Liquidity can be preserved without forgoing interest.

- Assigning emergency cash a specific role improves durability.

Why checking accounts feel like the safest place

Checking accounts are designed for immediacy. Funds are available instantly, balances are stable, and there is no friction to access cash. For emergency planning, this simplicity feels aligned with the goal: money should be there when needed, without delay or uncertainty.

This instinct is reinforced by risk avoidance. Emergency funds are not meant to fluctuate, and many investors equate earning interest with taking risks. As a result, checking accounts become the default - not because they are optimal, but because they feel unquestionably safe.

At first glance, nothing appears compromised.

Where the assumption breaks

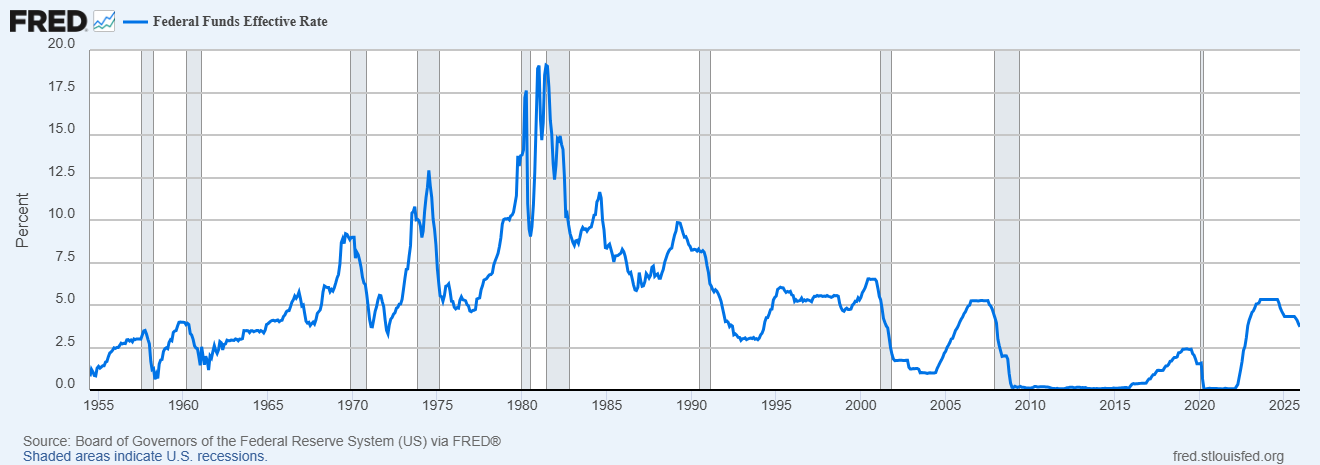

In periods when short-term interest rates rise, the economic cost of holding cash at zero yield becomes structurally visible.

This chart shows how short-term rates have periodically moved well above zero over time. When checking accounts fail to reflect these conditions, emergency cash preserves liquidity but forfeits real purchasing power and income.

The key distinction is between liquidity and location.

Checking accounts provide liquidity, but they are not the only vehicles that do. When emergency funds sit in accounts earning little or no interest, their purchasing power erodes over time, especially during periods of elevated inflation or higher short-term rates.

In recent market environments, many high-yield savings accounts and similar cash vehicles have offered annual percentage yields in the mid-single-digit range, with some offers around ~4–5% APY. By contrast, most traditional checking accounts and basic savings accounts continue to pay close to zero, making the difference in yield material over time and altering how much protection an emergency fund actually provides.

This is where the logic breaks: accessibility does not require inactivity.

How emergency cash quietly loses ground

Emergency funds are meant to be stable, but stability is not the same as neutrality.

When reserves earn nothing, inflation steadily reduces their real value. At the same time, foregone interest represents lost capacity to replenish or extend the buffer. The fund still exists, but it protects less than intended.

Because balances do not decline nominally, this erosion is easy to miss. Statements look unchanged. No visible loss occurs. The effect is cumulative rather than acute.

Over long periods, an emergency fund held entirely in a non-yielding account may no longer match the scale of the risks it was meant to cover.

Why does this inefficiency persists

Emergency planning is deliberately conservative. Investors are taught to prioritize access over return, and many interpret that guidance as a reason to ignore yield altogether.

There is also inertia. Once an emergency fund is established, it tends to be left alone. The account choice becomes part of the background, even as market conditions change and alternatives improve.

The issue is not misunderstanding the purpose of an emergency fund. It is assumed that the purpose requires accepting zero return indefinitely.

A More Durable Way to Frame Emergency Cash

Investors who manage emergency reserves more effectively tend to adopt a simple reframing:

Emergency funds should be liquid, not idle.

This perspective separates the function of the money from the vehicle holding it. Emergency cash remains immediately accessible, but it is stored in accounts designed to preserve value rather than quietly erode it.

The goal is not to maximize yield or take risk. It is to ensure that the fund continues to perform its protective role as conditions change.

Liquidity is the constraint. Yield is the opportunity.

When a checking account may still be appropriate

There are cases where holding part of an emergency fund in a checking account makes sense - such as covering very short-term contingencies, avoiding transfer delays, or simplifying cash management during transitions.

The distinction is scope.

Keeping a small, transactional buffer in checking is different from holding the entire emergency reserve there indefinitely. The mistake arises when convenience substitutes for intention.

Emergency funds work best when they are structured deliberately, not by default.

How optimized is your portfolio?

PortfolioPilot is used by over 40,000 individuals in the US & Canada to analyze their portfolios of over $30 billion1. Discover your portfolio score now:

The only Net Worth Tracker you need

Track all your assets in one place for free - no hidden costs and no credit card needed.

.webp)