5 Portfolio Analysis Strategies You Need to Know

Did you know that asset allocation plays a crucial role in long-term portfolio performance? Research by Brinson, Hood, and Beebower (1986) found that asset allocation accounts for approximately 80% of return variability over time. A later study by Ibbotson and Kaplan (2000) estimated that asset allocation explains about 40% of the differences in returns among funds. While these numbers vary significantly, both studies highlight that asset allocation is a critical factor in portfolio performance and should not be ignored.

Yet, many people check their portfolios by looking at their returns and calling it a day. But returns only tell part of the story. What about hidden risks, tax inefficiencies, fees, or investments that aren’t as diversified as they seem? A portfolio that looks great in a bull market could collapse when conditions change.

If you want to invest smarter and avoid nasty surprises, you need to dig deeper. Here are five powerful strategies that can uncover hidden risks and optimize your portfolio—some of the same techniques professional investors use.

Key Takeaways

- Looking at correlation helps reveal whether you’re truly diversified or just holding similar assets.

- Risk-adjusted returns show if you’re actually getting paid for the risk you’re taking.

- Stress-testing your portfolio helps prepare for market downturns before they happen.

- Tax-efficient investing can keep more money in your pocket.

- Rebalancing prevents your portfolio from drifting into a riskier position over time.

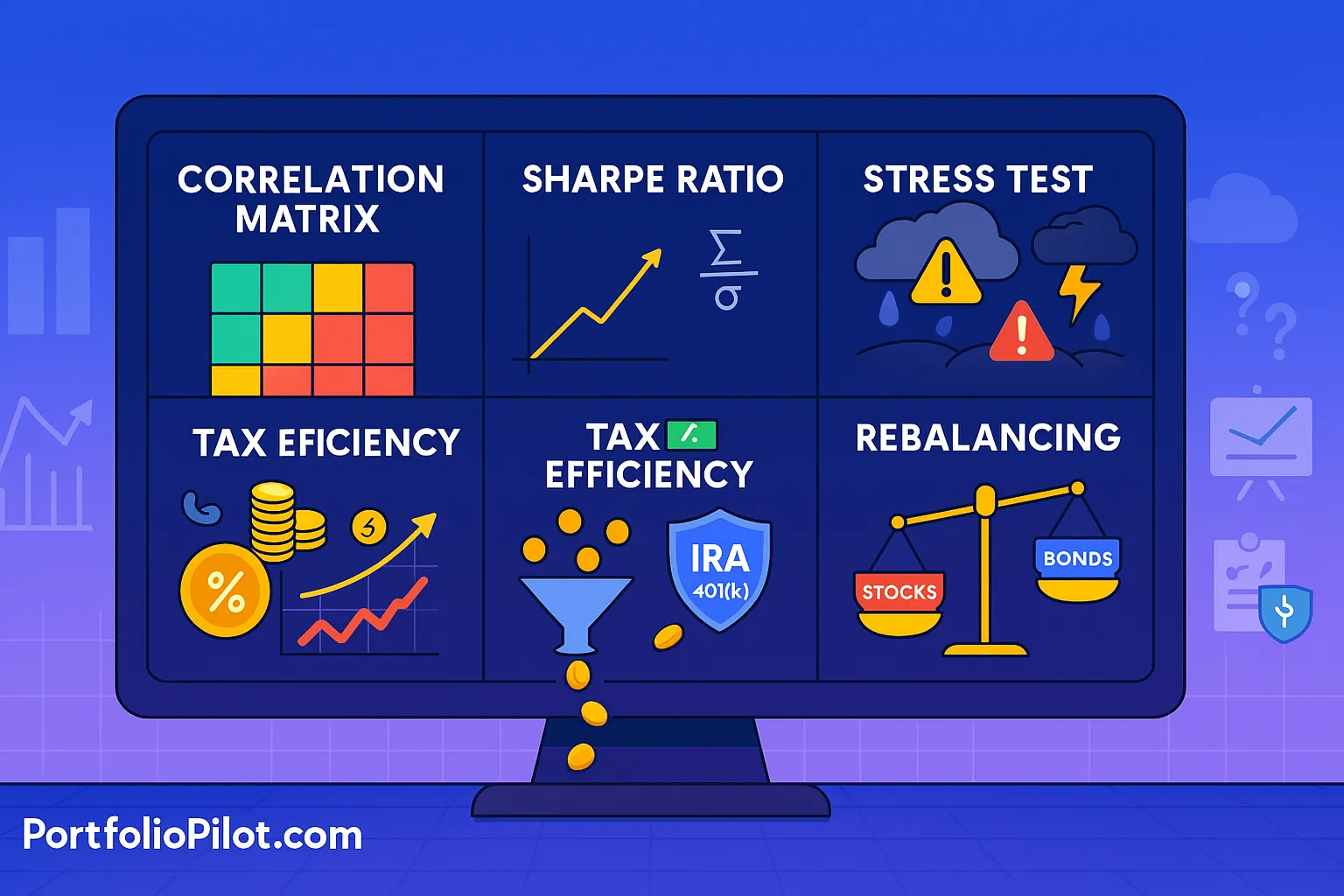

1. Correlation Analysis: Are You Actually Diversified?

You might think that owning different stocks, ETFs, and mutual funds means you’re diversified—but if those investments all tend to move together, you’re not really spreading out your risk.

How It Works:

Correlation measures how different investments move in relation to one another. A correlation of +1 means two assets move in perfect sync, while -1 means they move in opposite directions.

Why It Matters:

- If your assets are highly correlated, a market downturn could hit your portfolio harder than you expect.

- A well-diversified portfolio should have assets that perform differently in various market conditions.

Hypothetical Example: Imagine you own a tech ETF, a semiconductor stock, and a growth-focused mutual fund. At first glance, it looks diversified. But in a tech downturn or liquidity crunch, all three could drop at the same time.

One Possible Solution: Mix in low-correlation assets like bonds, commodities, or dividend-paying stocks to reduce overall risk.

2. Sharpe Ratio: Are You Getting Enough Returns For Your Risk?

It’s easy to focus on returns, but returns without context are meaningless. Two portfolios with the same risk level can have completely different returns. That’s where the Sharpe ratio comes in—it measures how much return you’re getting for the risk you’re taking.

Formula:

Where:

- Rp = Portfolio return

- Rf = Risk-free rate (e.g., U.S. Treasury yield)

- σp = Portfolio standard deviation

Why It Matters:

- A higher Sharpe ratio means better risk-adjusted returns.

- A low Sharpe ratio suggests you might be taking too much risk for the returns you’re getting.

- We think it is crucial to understand that you can increase your expected returns without changing the amount of risk you’re taking (almost sounds too good to be true…).

3. Stress-Testing: Can Your Portfolio Survive a Market Crash?

Would your portfolio hold up in a 2008-style financial meltdown? Stress-testing simulates extreme scenarios to see how your investments might perform in different crises.

Common Stress Tests:

- Historical events: Simulate how your portfolio would have performed in past crashes (dot-com bubble, 2008 GFC, COVID-19 selloff, etc.).

- Interest rate spikes: If you own bonds, how would rising rates affect your returns?

- Sector collapses: What happens if a major industry in your portfolio tanks?

Why It Matters:

A lot of investors assume they can handle risk—until they experience a major downturn. The psychological toll of not knowing how far down the numbers will go. The anxiety associated with your portfolio being down 40% and losing your job at the same time. Not to scare you, but sometimes when things get bad, they get really bad. Stress-testing shows you what could happen before it’s too late.

Hypothetical Example: A retiree with a 60/40 stock-bond portfolio runs a stress test and finds that in a severe market crash, their portfolio could drop 25% in a year. If they need that money soon, they might shift toward more defensive investments.

4. Tax Efficiency: Are You Losing Money to Taxes?

Even if your investments perform well, unnecessary taxes can quietly eat away at your profits. That’s why tax-efficient investing is so important.

Common Tax Mistakes:

- Holding high-yield bonds in taxable accounts (interest is taxed as income).

- Selling stocks too soon (short-term capital gains are taxed higher than long-term gains).

- Ignoring tax-loss harvesting, which can offset capital gains.

Possible Solutions:

- Keep income-producing investments (like bonds, REITs) in tax-advantaged accounts like IRAs or 401(k)s.

- Hold stocks for at least a year to qualify for lower long-term capital gains tax.

- Use tax-loss harvesting by selling underperforming stocks to offset taxable gains. This is not a year-end strategy, you can do this repeatedly throughout the year, taking advantage of market volatility.

5. Asset Allocation Drift: Is Your Portfolio Off-Balance?

Your portfolio’s original stock-to-bond ratio (or whatever asset allocation you chose) won’t stay the same forever. If stocks surge, your allocation might drift toward being too aggressive, exposing you to more risk than intended.

Why It Matters:

- If stocks have outperformed, you might be overexposed to risk.

- If bonds have outperformed, you might be too conservative, limiting future gains.

How to Fix It:

- Review your portfolio quarterly to ensure it matches your original allocation.

- Rebalance by selling overperforming assets and buying underperforming ones.

How optimized is your portfolio?

PortfolioPilot is used by over 40,000 individuals in the US & Canada to analyze their portfolios of over $30 billion1. Discover your portfolio score now:

Analyze your entire net worth

360° portfolio analysis, AI Assistant, and personalized recommendations guided by our Economic Insights Engine.