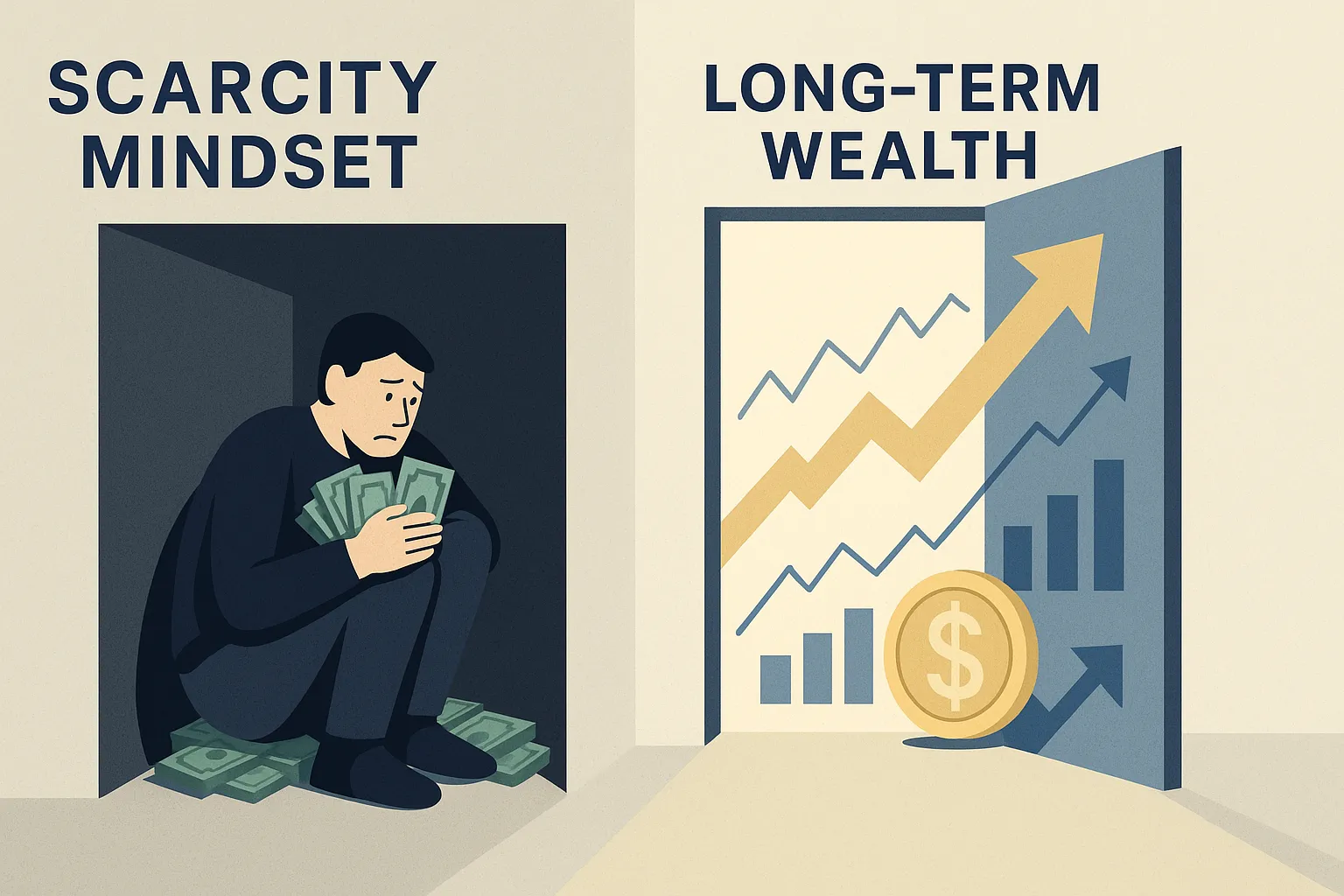

Is Scarcity Mindset Killing Your Investment Returns?

According to the 2023 study The Economics of Financial Stress by the National Bureau of Economic Research, financial stress can significantly impact individuals' economic decisions. While the study doesn't directly link financial anxiety to specific investment behaviors, it highlights how financial stress can influence consumption and labor supply decisions. Additionally, research from the American Psychological Association suggests that a scarcity mindset—where individuals perceive their resources as insufficient—can lead to prioritizing short-term safety over long-term growth, potentially affecting investment choices.

This article explores how scarcity-based thinking impacts investment decisions and how adopting a more resilient, abundance-oriented mindset may help investors avoid the traps that derail compounding wealth.

Key Takeaways

- The scarcity mindset triggers fear-based investing, like hoarding cash or avoiding risk entirely.

- Missing market upside may often hurt long-term returns more than enduring short-term losses.

- Behavioral traps rooted in scarcity include overtrading, panic selling, and under-investing.

- Mindset—not market knowledge— can often drive portfolio performance.

- Reframing risk and opportunity through structured planning can shift the equation.

What Is a Scarcity Mindset—and Why Does It Matter?

Scarcity mindset is a psychological pattern where a person views resources as finite and fragile. It stems from early experiences with instability or current perceptions of risk. In investing, this might often show up as:

- Holding excess cash “just in case”

- Avoiding equities or real estate due to fear of loss

- Obsessively checking portfolios

- Selling into downturns to avoid more pain

Hypothetical: Imagine a person who has saved $150,000 but keeps 80% of it in cash due to past volatility. Inflation quietly erodes value, and compounding is limited. Over 20 years, that decision may cost them more than any bear market ever could.

The Real Cost of Playing Too Safe

While market downturns are visible and dramatic, missed upside is the silent killer. According to Fidelity data (2023), missing just the 10 best-performing days in the S&P 500 over a multi-decade period can cut overall returns by more than 50%. Yet many scarcity-driven investors sit on the sidelines during recoveries, waiting for “clarity.” Fear-based strategies can often result in:

- Lower compound returns

- Weaker inflation protection

- Emotional burnout from constant uncertainty

So what? The long-term penalty for avoiding risk might often be steeper than the short-term impact of taking it.

Behavioral Finance Meets Mindset Psychology

Scarcity mindset overlaps with several well-documented behavioral finance traps:

- Loss aversion: The pain of losing $1 feels stronger than the joy of gaining $1

- Status quo bias: Fear of change keeps portfolios static

- Myopic loss aversion: Constant monitoring increases anxiety and reactive behavior

- Anchoring: Past bad experiences distort present decisions

These biases don’t disappear with more knowledge. They shift when people redefine their relationship to risk, abundance, and control.

Shifting From Scarcity to Strategy

A scarcity mindset doesn’t mean someone is “bad with money.” May often, it’s a sign they’ve never been taught to think in systems or time horizons. Strategies that help:

- Use financial planning tools to visualize long-term outcomes

- Automate investing to reduce decision fatigue

- Define capital purpose buckets: emergency fund, growth capital, future spending

- Anchor risk to goals—not market noise

Hypothetical: A person invests 70% of their savings in a diversified portfolio, with 30% in cash for near-term needs. This structure satisfies their need for safety—without sacrificing long-term growth.

With the right framework, even risk-averse investors can build a plan that feels safe and grows wealth.

Scarcity Is Emotional—So Is Confidence

Money is rarely just math. For many investors, financial decisions are proxies for deeper concerns—security, identity, or control. Scarcity-based decisions may feel responsible—but they can often reflect unexamined emotion, not informed risk management. Long-term confidence comes from knowing:

- There’s a plan, not just a portfolio

- Risk is intentional, not accidental

- Money has purpose—not just protection

And ironically, that’s what allows people to take more risks, more calmly—because it’s aligned with something deeper than just fear.

A mindset worth building: Investors who view capital as a tool—not something to hoard—tend to build more durable wealth over time. The key shift? From “What if I lose it?” to “How do I use it?”

How optimized is your portfolio?

PortfolioPilot is used by over 40,000 individuals in the US & Canada to analyze their portfolios of over $30 billion1. Discover your portfolio score now:

Analyze your entire net worth

360° portfolio analysis, AI Assistant, and personalized recommendations guided by our Economic Insights Engine.