Retirement Planning: PortfolioPilot vs Empower Retirement

According to the Social Security Trustees, the combined trust funds are projected to pay scheduled benefits in full until 2034, after which about 83% of benefits may be payable if no changes are made (SSA, 2025). At the same time, inflation spiked to a 9.1% 12-month increase in June 2022 before easing, reminding retirees that purchasing power can swing quickly (BLS, 2022). Many investors assume a one-time calculator is enough. The real challenge is building a plan that adapts to changing markets, taxes, and personal milestones. This article explains how PortfolioPilot and Empower Retirement approach that problem differently, and what those differences mean for long-term planning, account integration, and day-to-day usability.

Key Takeaways

- PortfolioPilot provides free, ongoing, tax-aware retirement planning connected to diversification, fees, and estate modules.

- Empower offers two experiences: workplace retirement plan tools and the Empower Personal Dashboard, which includes a free Retirement Planner.

- Both platforms support projections and account linking, but PortfolioPilot emphasizes multi-asset coverage and adaptive, monthly updates, while Empower’s experience differs depending on whether the user is inside an employer plan or using the consumer dashboard.

What Both Platforms Offer (10 Shared Capabilities)

- Retirement projections - Both tools estimate retirement readiness and income sustainability.

- Scenario modeling - Each allows “what-if” testing, such as adjusting retirement age, savings rate, or spending assumptions.

- Goal tracking - Progress visualizations help users monitor how current behavior aligns with future goals.

- Account aggregation - Both allow the connection of multiple accounts for a consolidated financial view.

- Multi-asset inclusion - Portfolios can include brokerage, retirement accounts, and real estate holdings.

- Tax-sensitive planning - Each factor in the difference between taxable and tax-advantaged accounts.

- Inflation adjustment - Projections account for changing purchasing power over time.

- Holistic dashboards - Centralized visuals for assets, liabilities, and income streams.

- Behavioral insight - Designed to reduce reactive decision-making by offering structured feedback.

- Educational context - Both platforms provide learning resources to support more informed planning decisions.

So what? Both build retirement forecasts, but PortfolioPilot integrates broader coverage and automation, while Empower organizes around plan-centric tools.

Turn your retirement assumptions into concrete, model-driven scenarios.

Free vs. Paid: The Key Divide

- PortfolioPilot

- Free for individuals: Offers retirement projections, scenario testing, tax-aware insights, and diversification analytics at no cost.

- Optional flat-fee membership: Adds continuous tax optimization, fee monitoring, and estate workflow integration.

- No AUM or management fee: Investors maintain full control; guidance operates independently of asset custody.

- Empower

- Free workplace tools: 401(k)/403(b) participants can access retirement readiness projections and contribution guidance within their plan portal.

- Free consumer dashboard: Empower Personal Dashboard (formerly Personal Capital) includes a Retirement Planner and account aggregation tools at no cost.

- Paid advisory option: Empower Advisory Group, an SEC-registered investment adviser, offers managed portfolios for a percentage-based fee typically ranging from about 0.49% to 0.89% of assets under management, depending on balance tier. Advisory fees apply separately from the free dashboard experience.

So what? PortfolioPilot gives unified, ongoing guidance without asset-based fees; Empower combines free planning dashboards with optional professional management.

Where They Differ (and Why It Matters)

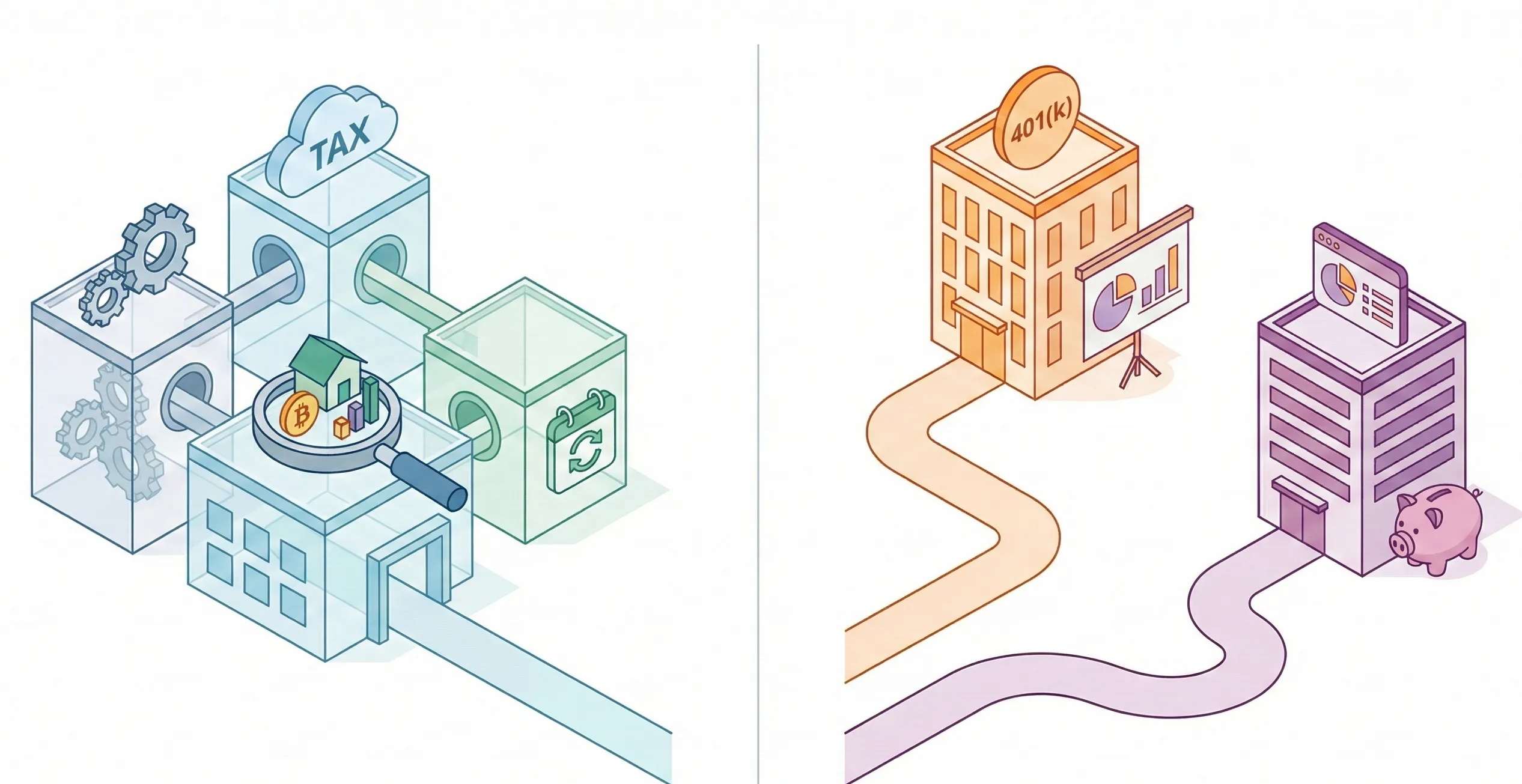

PortfolioPilot - Integrated, Adaptive Planning

- Monthly updates: Plans refresh automatically based on market data, tax events, and account changes.

- Multi-asset coverage: Models real estate, retirement, brokerage, crypto, and cash in one plan.

- Tax-aware modeling: Distinguishes taxable vs. tax-advantaged accounts for more realistic withdrawal timing.

- Diversification & estate linkage: Connects retirement outcomes to broader risk and planning modules.

Empower Retirement - Split Ecosystem

- Two user paths: Workplace participants use employer-linked planning tools; consumers can access the free Personal Dashboard.

- Goal-based projections: The Retirement Planner lets users adjust inputs like savings rate or retirement age interactively.

- Account aggregation: Free dashboard connects external holdings for a household-level view.

- Optional advisory services: Managed accounts through Empower Advisory Group with associated AUM fees.

Which Platform Fits Different Planning Styles?

- Choose PortfolioPilot if you want integrated, adaptive planning that connects retirement, tax, and diversification guidance with automatic monthly updates - without asset-based fees.

- Choose Empower if you already have a workplace plan through Empower or prefer separate dashboards for employer accounts and broader household tracking.

The comparison is based on publicly available information from each provider’s website as of 11/19/2025. Features, fees, and methodologies may change over time. Platform features, pricing structures, and planning methodologies may evolve over time, which can affect how projections and guidance are generated.

How optimized is your portfolio?

PortfolioPilot is used by over 50,000 individuals in the US & Canada to analyze their portfolios of over $40 billion1. Discover your portfolio score now:

An easy way to plan your financial future

PortfolioPilot helps you plan and achieve your retirement goals, with financial models that predict your retirement success and calculate the taxes involved.

.webp)